Valuations are rising & the HMRC SAV team is as intelligent at ever

May 7, 2024

The good performance of UK stock markets is already making a difference to private company valuations.

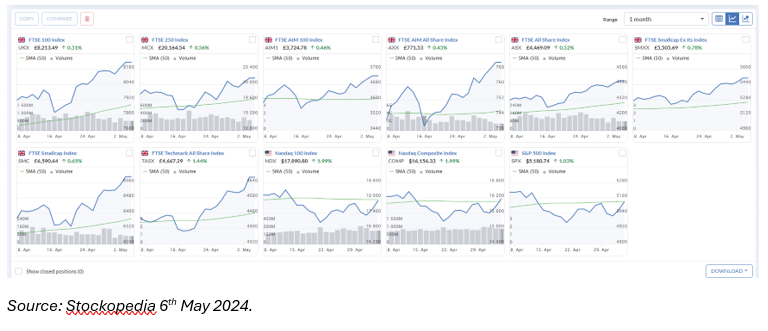

I do love a good chart. A picture speaks a thousand words. I thought you might like to see the performance of the main UK indices against the main US ones, as relative performance over the last month is leading to some interesting thinking on how this could impact on private company valuations.

As you can see the UK indices are all trending up, some of them quite significantly. In contrast the main US indices are showing signs of stress.

What does this mean for us? When we are conducting a valuation we frequently seek out comparable quoted companies to obtain multiples and then we consider discounts for matters such the size of the company and relative illiquidity. We also have to think about the markets where the comparables are trading. What if the comparables are based in the US but we are valuing a UK company? If the US market is trading on a higher multiple than the UK market we have to think about that issue.

However it looks as if the multiples in the US and the UK may be beginning to convergence. Time will tell.

There’s a debate raging in the valuations world about whether the listed market price of a liquid stock has a premium in it such that the multiple should be discounted when applied to a private company share. After all, we know that in M&A, bidders for listed stocks tend to pay a premium to take the company off the market. Of itself that suggests that the premium did not exist in the share price before the bid was made.

Some argue that the market price simply comprises 1,000s of uninfluential minority trades. If one agrees with this view, clearly you should not discount the multiple.

We are still mulling this thesis. I can’t help feeling that even if the thesis is technically correct, there should be a premium for the ability to ring a stockbroker and sell or buy immediately. I also think not enough is discussed around the relative size of a small private company to a large listed one. Unless you are in PE-backed buy-and-build mode, most acquirors would, I think, prefer to buy something that has greater size and firepower if they can and that commands a premium surely?

Then there is the issue of information. Public companies have to publish A LOT of information. The largest have dozens of analysts following them who can also provide a view. And that’s before one gets into the chatrooms which abound all over the internet. In theory all that transparency means a company should be fairly priced and certainly compared to a private company, where information is not readily available or may be less complete.

If you agree that transparency reduces risk, then surely quoted companies are less risky than private companies?

The truth, of course, remains that each case is unique. Maybe the private company is actually larger than the listed comparables, or perhaps it is unusually transparent in telling the world about how it is performing?

The good news, if you are a UK based company, is that quoted comparable multiples are improving and that will drag private company valuations up.

It does mean, however, that it sets higher base line for valuation. When it comes to growth shares in particular, this means that, for example the hurdle may have to become more stretching to increase the risk to the shares flowering, such that the value can reasonably be denuded to a price that the individual is willing to pay. Growth shares are never worth par value just because one wants them to be. It must be provable that their value is low for justifiable reasons such that the risk to them returning a profit is very remote indeed.

I went to the HMRC SAV team’s latest industry seminar on Friday. I can report back that these people are seriously clever. As they said to us valuers, “you should do your job properly. We will then see if we agree with you.” They do not think valuations can be standardised or automated. They do not see it as their job to provide precedents or rules. What that means is that if your clients do not get a proper and thorough job done in a valuation exercise, they are leaving themselves seriously exposed to a challenge at some point from people who really know what they are doing.

If there is a void in the maths and the arguments to justify the valuation, HMRC – quite reasonably – could start asking some pretty pointed questions about claims made as to value.

So do warn your clients that comprehensive valuation reports really do reduce the risk of a tax enquiry. (Funnily enough we are talking right now to someone about whether he can resist a claim for several £ms in tax from HMRC. The claim has come precisely because no-one bothered to do a valuation, let alone get an independent valuation to validate it, for a share transfer some years ago).

Do call if one of your clients has a question about how stock market performance can affect a valuation. And if you know of any share or asset transactions that took place in the past without an independent valuation, it might be wise to suggest your clients obtain a historical valuation to pre-empt or prepare for a tax enquiry.